Taming the Taper Tantrum

How Indonesia handled an economic crisis — and what the current administration should learn from it

As the rupiah plummeted, Indonesians nationwide have organized protests expressing discontent with the government’s handling of the country’s worsening economy. Can Indonesia get out of this rut?

Economists have warned since last year to rectify the disproportionate budget for populist programs like the flagship Free Nutritious Meal (MBG) program. Some argue that the Indonesian central bank, Bank Indonesia (BI), should intervene to stabilize the rupiah. While they are all good recommendations, we thought it would also be a good idea to look back in history to see whether we have been through a similar crisis and how we handled it.

Turns out, once upon a time, we actually did rescue ourselves from an impending economic crisis.

In 2013, Indonesia faced an economic crisis after the United States Federal Reserve (‘The Fed’) signaled it would begin tapering its bond-buying program. This move sent shockwaves through the developing world, triggering capital outflows, currency depreciations, and tumbling financial markets in what became known as the Taper Tantrum.

Indonesia was among the hardest-hit, joining Brazil, India, South Africa, and Turkiye as countries dubbed the “Fragile Five” — a group perceived as most vulnerable to the Fed’s tapering policy. Incredibly, Indonesia made its way out of the “Fragile Five” in just seven months.

How did we do that? In this edition of The Reformist, we uncover how Indonesia lifted itself from the brink and what lessons the Prabowo administration would do well to heed today.

Growth under borrowed time

Much like the United States-Iran war, the Taper Tantrum was a sudden, unexpected phenomenon that caused global panic. After the 2008 global financial crisis, the US entered a Great Recession. The Fed then stepped in to revive the economy through Quantitative Easing (QE).

Given a deflationary US economy, everyone was afraid to spend. So, the Fed purchased assets and bonds from US commercial banks in exchange for dollars, thereby pouring more money into the US financial system. This, in conjunction with lowering the interest rate, led people to spend more, reviving the sluggish economy.

The effects of the US’s domestic policy reached Indonesia precisely because of this influx of new capital. With low interest rates, US dollar-holding investors began to look to emerging countries like Indonesia for higher returns on their investments.

From 2009 to 2014, external financing to Indonesia (bonds, equities, and loans) increased from US$ 24.7 billion to US$ 32.6 billion, peaking in the second quarter of 2013, just before the crisis ensued. Globally, emerging markets received close to half of all capital flows during this period, with roughly 90 percent of that concentrated in just eight countries; Indonesia among them. Critically, much of this inflow exceeded what Indonesia’s economic fundamentals could actually justify.

This led to what former Finance Minister Chatib Basri labeled a “false normal world.” The post-2008 flow came with an incredible wave of new capital. But even he understood that the numbers were unsustainable. During this period, the rupiah appreciated sharply against the dollar.

Additionally, the economist noted a lack of investment in the country’s export-oriented sector, with investment instead directed towards the highly volatile commodities sector. The former would have created industries meant for long-term economic growth (factories, manufacturing, traded goods), whereas the latter is a short-term cash grab that gets transferred out of the country as soon as commodity prices spiral. Indonesia was getting richer during this period, but doing so on a fragile foundation.

Normal, on the other hand, is a world without QE. When the Fed signaled in May 2013 that it was preparing to wind down its QE program, the world snapped back to normal very quickly. Investors who had been chasing returns in emerging markets suddenly had reason to bring their money back to the US.

For Indonesia, the consequences were swift and severe: the rupiah plummeted, the stock market collapsed, and foreign exchange reserves began to drain.

The Taper Tantrum had arrived.

Preventing monetary lift off

Just days before the Fed signaled that it would reverse the QE policy, Chatib Basri was appointed finance minister by then-President Susilo Bambang Yudhoyono (SBY) to oversee the appropriation of the 2014 state budget. But when the Taper Tantrum began, all focus shifted to handling an impending economic crisis.

The most crucial aspect of taming the market during the period was to prevent panic selling of the rupiah. The government did so by applying a variety of monetary policies through central bank intervention. BI pulled three levers in quick succession: hiking the policy rate, tightening liquidity conditions, and, critically, pulling back from excessive foreign exchange market intervention.

On the rate front, BI increased its policy rate by 175 basis points to 7.25 percent and raised the overnight deposit facility rate — the rate at which commercial banks receive for parking their money in BI — to 5.5 percent. Higher interest rates make holding rupiah-denominated assets more attractive to investors, since they now earn better returns, slowing the rush toward the exit.

The intuitive assumption is that a weakening rupiah is driven by businesses and individuals rushing to buy dollars to avoid a crash. This is true if those dollars leave Indonesia. But if the dollar remains within the country’s banking system, the pressure on the exchange rate is cushioned, making it easier for the central bank to manage.

To keep dollars in the system, BI introduced biweekly foreign-exchange swap auctions with commercial banks, giving businesses a way to hedge their dollar exposure without physically taking dollars out of the country. It also gave banks broader maturity options, or the liberty to choose how long they would like to park their US dollars with BI, making it more attractive to keep dollars in the Indonesian financial system.

The most counterintuitive decision, however, was what BI chose not to do. Before the crisis even occurred, BI had been burning through its foreign exchange reserves to artificially prop up the rupiah.

Chatib, along with the then-trade minister, Gita Wirjawan, argued and eventually convinced President SBY that this had to stop. The rupiah needed to be allowed to weaken in line with market fundamentals, rather than be defended at great cost.

Once BI stepped back from excessive intervention, reserves began to stabilize and eventually recover, climbing from a low of US$ 92 billion in August 2013 back to US$ 99 billion by the end of December and US$ 105 billion by April 2014.

But the decision to let the rupiah weaken was not merely about conserving reserves. It was also a deliberate policy tool in its own right. Economists call this expenditure switching, a policy in which the government attempts to shift consumption of foreign goods towards domestic goods. The way it works is that when a currency weakens, Indonesian exports become cheaper for foreign buyers, making them more competitive in world markets. At the same time, imports become more expensive for Indonesians, nudging domestic consumers toward local products.

One prudent lesson from the Taper Tantrum crisis was that BI could wield its monetary policy decisively, even if it meant sacrificing short-term economic growth.

Today, there is a perception that BI is under pressure to support the administration’s political agenda. This is evidenced by the “burden-sharing” arrangement, in which BI revives pandemic-era bond purchases to finance populist programs, effectively amounting to debt monetization and fiscal dominance. Last year, economists warned that this scheme could threaten BI’s independence, currency stability, and investor confidence.

And then there is the recent revision to the Financial Sector Development and Strengthening Law (UU P2SK), which now expands BI’s role to support economic growth. But even before UU P2SK was passed, BI had cut the policy rate three times last year, from 5.75 percent at the start of the year to 4.75 percent by the end of the year. Much like what the Fed did: with a lower interest rate, borrowing becomes cheaper, but saving becomes less attractive.

This is good for a pro-economic growth administration like Prabowo’s, as more capital can be used to support the government’s policy agenda, whether flagship or infrastructure programs. But it can be incredibly detrimental to the rupiah’s strength, as the currency becomes less attractive to hold for investors. What serves the government’s growth agenda, however, does not necessarily serve the rupiah.

Now, everyone has felt the effects of a weakened rupiah, despite President Prabowo’s claim that “villagers do not use the dollar”. Importing foreign goods has become increasingly expensive, raising the prices of everyday staples and — widely covered by the media recently — pharmaceutical products, impacting public health services and people with chronic illnesses.

After the US-Iran war erupted in February, BI still maintained the 4.75 percent policy rate through May. It was only after the rupiah exceeded Rp 18,000 and persistent external pressure that BI decided it was time to intervene in the interest rate. On 20 May, BI raised it to 5.25 percent, and only a week ago to 5.5 percent.

As soon as the hikes were implemented, the rupiah slowly recovered and dropped below Rp 18,000, signaling a return of market confidence and highlighting the need for monetary prudence amid geopolitical uncertainty.

Ripping the necessary fiscal band-aid

Monetary policy alone, however, would not have been enough to close the wound. During the Taper Tantrum, the deeper structural problem was Indonesia’s current account deficit (the difference between what the country earned from exports and what it spent on imports), driven specifically by fuel subsidies.

The government was subsidizing petrol and diesel prices so heavily that it was encouraging overconsumption, inflating demand for oil imports, and blowing out the budget. By 2013, if left unchanged, internal Finance Ministry estimates projected that the budget deficit would balloon to 5 percent of GDP, well above the 3 percent legal ceiling.

In a meeting with President SBY, Chatib lobbied that the current account deficit must be addressed through expenditure reduction, namely by reforming fuel subsidies. This was highly unattractive at the time, especially with the 2014 presidential elections right around the corner. The vast majority of Indonesians use petrol daily for personal and business consumption, so even a slight price hike would trigger a political uproar.

But the SBY administration was brave enough to rip the band-aid. In June 2013, following heated parliamentary debate and nationwide protests, the prices of subsidized petrol and diesel were increased by 44 percent and 22 percent, respectively. To cushion the blow, the government directed Rp 9.3 trillion from the savings toward direct and conditional cash transfers to 15.5 million low-income households, as well as Rp 7.2 trillion towards rural infrastructure spending.

In his testimony, Chatib cited a 2012 World Bank report which estimated that a fuel price increase of roughly Rp 1,500 per liter would push an additional 0.7 percent of Indonesians into poverty. Thus, fuel subsidy reform, in any capacity, has to be backed with progressive shock measures that take lower-income citizens into account.

Fast forward to 2026, and similar policy efforts seem to be underway in a poorly designed manner.

Just a few days ago, state energy company Pertamina hiked the price of non-subsidized petrol from Rp 12,300 to Rp 16,250 overnight. This followed the previous price increase, which occurred a couple of months earlier in March.

For economists, the increase was expected, given that the price of crude oil rose sharply from around US$ 57 per barrel at the start of the year to over US$ 120 per barrel at the peak of the US-Iran War in April. This is reflected in the state budget, which projected only that crude oil prices would hover between US$ 70 and US$ 95.

Yet, even if it was to be expected, public communication for this policy has been lackluster. The price increase happened overnight, without warning, and came not from the President but from an announcement by Pertamina’s subsidiary, Pertamina Patra Niaga. Talks of a new direct cash transfer program also came from National Economic Council (DEN) head Luhut Pandjaitan, who was called to the Presidential Palace for a completely different agenda.

Meanwhile, at his latest public address, President Prabowo showed no qualms about mentioning the price hike. Instead, he continued to mock dissent by calling on attendees to ignore those who snide at the government, insinuating his infamous rhetoric about foreign stooges.

Like Prabowo, then-president SBY was not brave enough to announce the price increase himself. But many of his ministers stepped in to assure the Indonesian public that they would be compensated, including Finance Minister Chatib Basri and Coordinating Economic Affairs Minister Hatta Rajasa.

Notably, the SBY administration had already warned the Indonesian public about a price hike for months, even before the Taper Tantrum, which assured the finance minister that fuel subsidies had to go.

They understood that managing a crisis was as much about managing perception as about managing the budget, especially for a politically sensitive issue like the fuel subsidy.

That lesson, it seems, has not made the trip from one administration to the next.

Lessons for the present day

Learning from this experience, Indonesia should be able to overcome today’s economic spiral despite widespread signs of pessimism. The key, however, lies in whether the current administration is willing to show enough humility and take the necessary steps to address systemic policy gaps.

As Chatib employed policy mechanisms in 2013, the same framework can be applied today to reverse the trend. In fact, in his recent public appearance at the Grab Business Forum, he provided a glimpse into the country’s current economic outlook.

He mentioned that the role of the finance minister is simple: either to earn more revenue, spend less, or borrow more money to ensure the stability of the Indonesian economy. Easier said than done, but entirely possible given the government’s ability to stabilize the economy a decade prior.

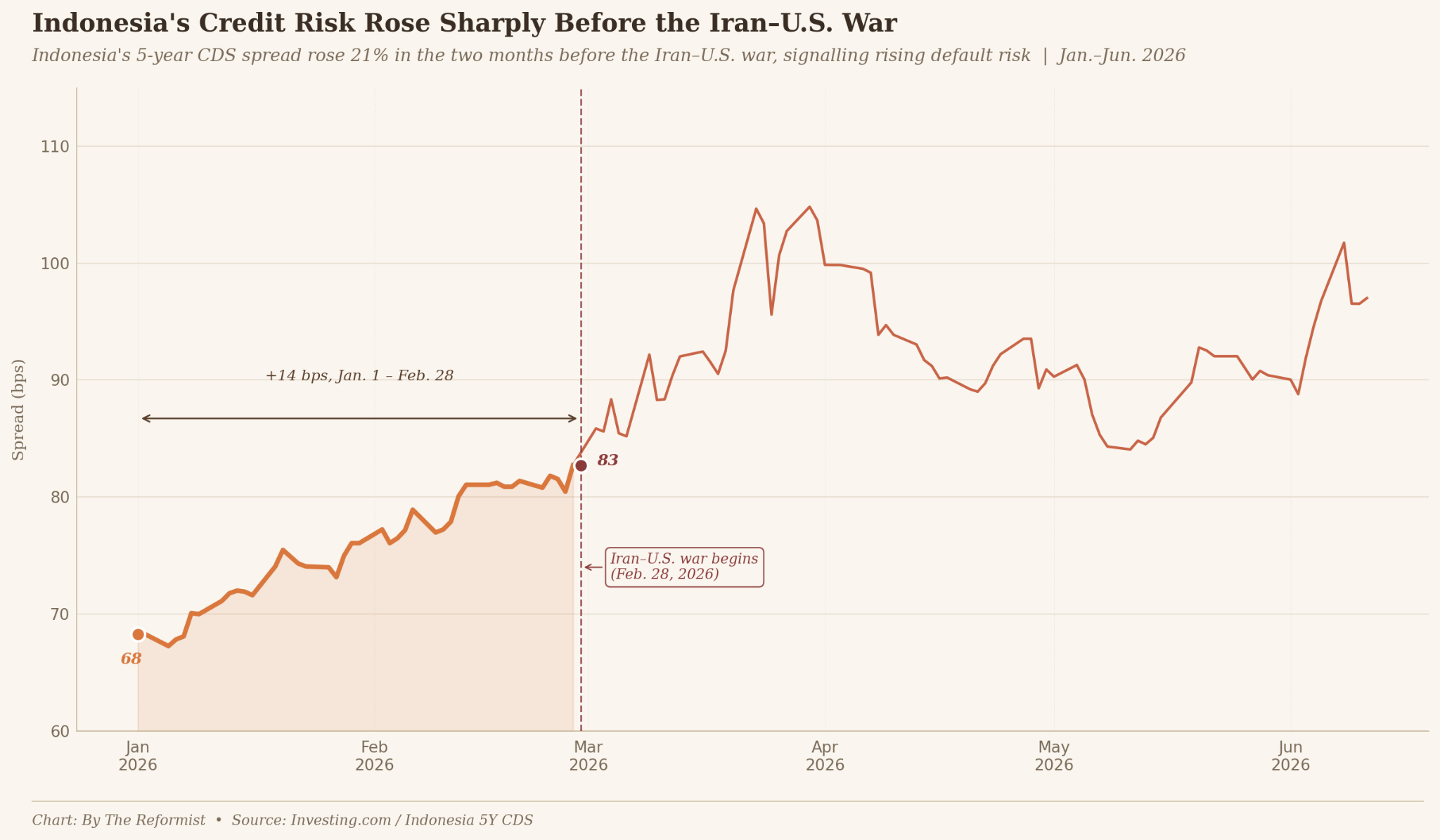

In his diagnosis, Chatib also pointed to Indonesia’s rising Credit Default Swap (the premium a lender pays to protect itself against the risk that a sovereign entity defaults on its loans) well before the war between the United States and Iran erupted. Take a look at this graph:

At the start of January this year, the CDS stood at around 68 basis points (bps). By the end of February, right before the US-Iran war started, that number jumped to 83 bps, up 14 bps, or roughly 22 percent.

This meant that even before the war brought about an oil crisis, foreign lenders had already begun to lose confidence in how the Indonesian government was carrying out its policies, to the extent that they were willing to pay a higher premium to protect themselves against the risk that the government might fail to repay its loans.

But the CDS serves more as a perception-based insight than as a reliable reflection of whether Indonesia will spiral into a great recession. It means the higher the CDS, the more foreign investors perceive Indonesia as riskier to invest in than before; nonetheless, they remain willing to invest in the country if they are better protected.

For the government, as Chatib explained, the rising CDS cannot be attributed to external factors alone. Rather, it is a reflection of questionable domestic policies that have strained capital trust.

External shocks are one thing. But what matters more is that investors want to see clean and prudent governance. Instead, they see the problematic implementation of the state-budget-straining Free Nutritious Meal (MBG) program, the rent-seeking tendencies of the centralization of commodity exports, and the increasingly prevalent criminalization of policymakers.

The Taper Tantrum was just as unexpected as the US-Iran War. Yet the government was willing to make unpopular decisions quickly and communicate them honestly to ensure long-term stability of the Indonesian economy.

In 2013, Indonesia surprised the world. Whether it can do so again depends less on the complexity of the policy tools available and more on the political will to use them.