Sun’s out, panels up: five clouds to clear towards Prabowo’s 100-gigawatt dream

Can Indonesia deliver this energy revolution vision?

Prabowo Subianto is a man of ambition. We get it. From the Free Nutritious Meal Program to 80 thousand village cooperatives, the President has been proclaiming sensational numbers that seem too good to be true. Most of the time, it invites skeptical glares. But if there’s a goal we can actually get behind, it would be his proposal to develop 100 gigawatts (GW) of solar energy in the next 10 years—especially if it opens the door for a potentially progressive and inclusive transition towards energy sovereignty.

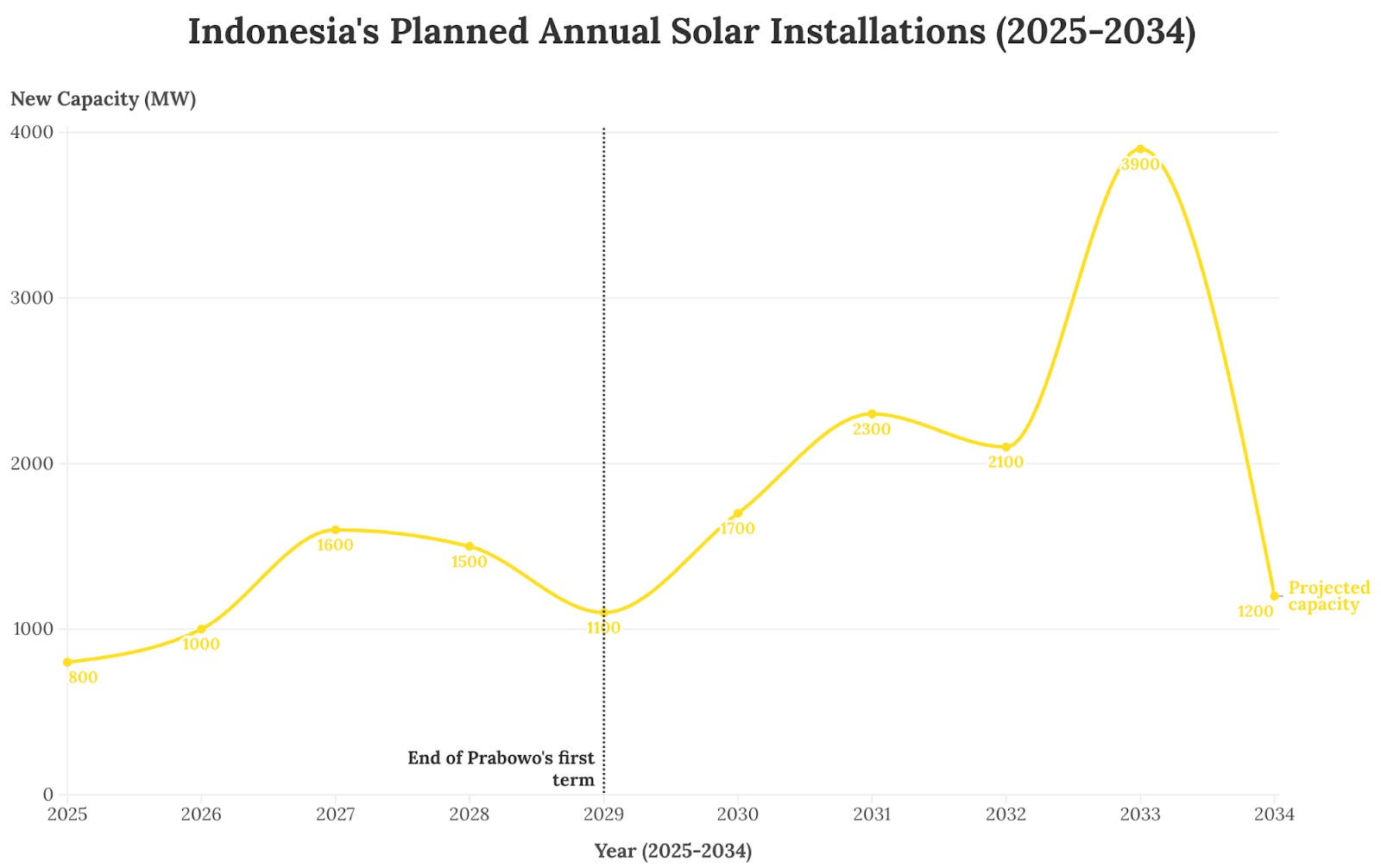

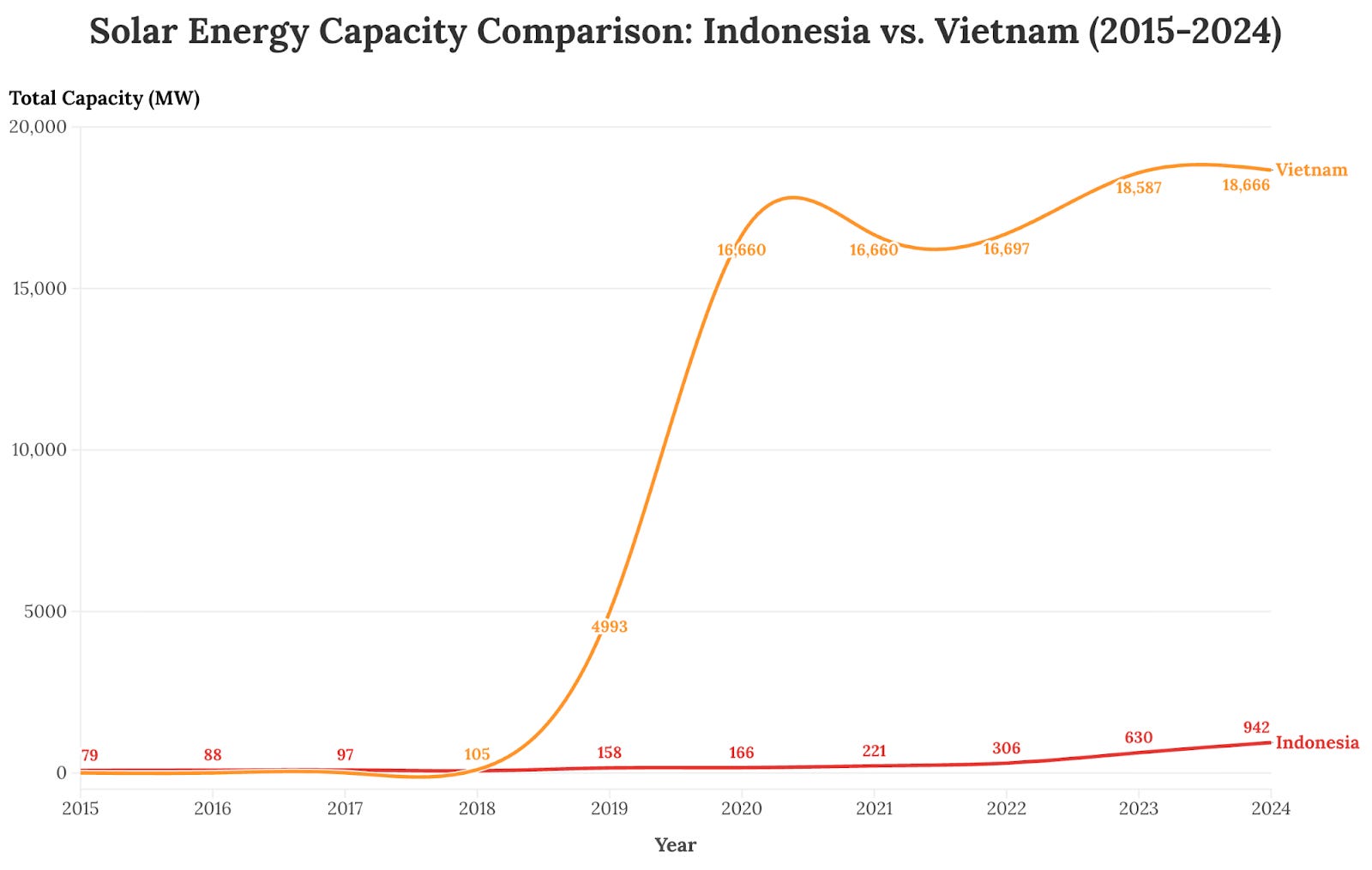

How ‘big’ is this target, exactly? Given Indonesia’s current 1 GW of installed solar energy, this ambition translates to a 100-fold increase in capacity. Between 2015 and 2024, Indonesia has only been able to increase its capacity from 79 to 942 megawatts (MW). This time around, the plan is to combine a centralized-decentralized approach, with 80 GW dispersed at 1 MW increments throughout 80 thousand villages, and the other 20 GW created through central government control.

Are plans already in place? To date, no official roadmap explains how this will be delivered. In addition, this target coexists with PLN’s 2025–2034 National Electricity Supply Business Plan (RUPTL), which aims for 17.1 GW of solar energy over the next decade—roughly 68% of which is going to extend beyond Prabowo’s first term in office. It remains a question how these two targets will reconcile.

So why are we doing this in the first place? The obvious reason is that this transition is essential to achieve Indonesia’s Net-Zero Emissions target by 2060. But it also makes sense economically: solar technology has reached the lowest production cost in history, making it cheaper than any other source of energy.

The proof? Everyone else has been picking up the pace. Countries like India went from 5.6 GW (2015) to over 135 GW (2025). China, a pioneer of the solar energy boom, increased its solar capacity from 43.5 GW (2015) to over 887 GW (2024). Both countries now top the list of the world’s largest solar energy producers alongside the United States. In Southeast Asia, Vietnam increased its solar energy capacity by 3,733 percent—from a mere 5 MW (2015) to over 18.6 GW (2024).

In this edition of The Reformist, we unpack Indonesia’s energy sector and outline what must change for a solar energy revolution to begin:

1. Stop making coal artificially cheap

Currently, the pricing point of solar-based energy is not yet competitive. Not because it is inherently expensive, but because its main competitor—coal—is kept artificially cheap. The Domestic Market Obligation (DMO) model mandates coal mining companies to sell 25 percent of their production at a capped price of US$70 per ton, much lower than the international standard of US$100 per ton. With rising coal production over the last five years, companies appear more than willing to abide by this as they remain competitive in global markets. Meanwhile, the government is already spending north of Rp200 trillion in electricity subsidies and compensation in 2025 alone.

Yet even as renewables operate under no such advantage, ongoing projects do indicate encouraging signs. The Cirata Floating Solar Power Plant, for example, operates at around US$5.8 cents per kWh, signalling that solar is approaching—if not already reaching—cost competitiveness amid heavy subsidies.

If Indonesia is serious about accelerating solar deployment, its falling production costs should be complemented by demand-side subsidies. India, for instance, offers an effective precedent through its Renewable Consumption Obligation (RCO), which mandates that a growing share of electricity consumption—43 percent by 2030—must come from renewable sources.

2. Tackle the intermittency and distribution problem

While being on the equator, Indonesia is not completely free of the intermittency challenge. Due to long periods of monsoon season, it enjoys a limited amount of sunlight in a year. To get ahead of this, Battery Energy Storage Systems (BESS) should be included in any solar project to store and generate electricity when sunlight is absent. To the administration’s credit, it has promised that for every 1 MW of solar capacity in every village, 4 MW of battery will be installed.

Given Indonesia’s archipelagic nature, another inherent challenge is distribution, especially to remote areas in the outer islands. The government seems to be adamant that 80 of the 100 GW capacity be delivered through 80 thousand village cooperatives because of operational feasibility concerns. These align with the need to plan microgrids, create new demands that do not compete with coal on larger grids, and mitigate the slow pace of coal-fired power plants’ early retirement.

3. Consider the economics of scale

Taking lessons from India and China’s solar booms, capacity expansion is more affordable when driven primarily by centralized large-scale solar projects. In India, around 85.7 of the 135 GW installed solar capacity comes from large-scale grid-connected plants. China goes even further: it hosts more such projects than any other country and, in 2024 alone, added 277 GW of new utility-scale solar capacity.

The argument for scale is an economic one. India’s Bhadla Solar Park operates at $3.7 cents per kWh with a 2 GW capacity and 56-square kilometers plant. The early success of Cirata Floating Solar Park is also similarly enabled by its scale.

Simply put: The larger the solar power plant, the cheaper the costs will be. With scale, Indonesia could potentially achieve a production cost much cheaper than the price cap set under Presidential Regulation No. 112/2022, where solar projects with capacities of up to 1 MW are subject to the highest price ceiling of US$11.47 cents per kWh, while projects exceeding 20 MW are capped at US$6.95 cents per kWh.

4. De-risk private investment, don’t strain the state budget

While village cooperatives are mandated with the development of solar initiatives, there remains no clarity on additional budget allocation, causing more questions on how exactly the government will help fund the initiative. The current scheme revolves around greater involvement of state-owned banks to lend capital into the project and the use of Rp240 trillion in government funds as liabilities for repayment.

State finances aside, this 100 GW dream doesn’t have to come at the expense of straining the state budget. Instead, foreign investment can play a role in realizing this ambition. There is no need for new innovative financing schemes to woo new investors. They will inject capital when risks can be calculated and given the security that their projects won’t incur losses from factors out of their control.

De-risking projects can take the form of clear and enforceable Power Purchase Agreements (PPA), aided land acquisition, streamlined permitting processes, and state-backed guarantees that shield projects from sudden regulatory shifts. Threats from non-state actors should also be accounted for. It shouldn’t be the case that solar farms are subjected to extortion in the same way an electric vehicle manufacturing factory was threatened in Subang, West Java. Eradicating these ‘hidden fees’ will substantially reduce capital expenditure and increase investor confidence.

5. Untangle the wire of state control in the electricity market

PLN is the only utility company that exists in the country and holds complete control over the Indonesian energy sector. This is by design and, from an idealist perspective, for good reason. The state views electricity as an essential commodity and public good, taking the sole responsibility for distributing it to every Indonesian at an affordable price. Across the four functions of generating, transmitting, distributing, and retailing electricity, private companies are only allowed to generate, while the rest is essentially monopolized by PLN.

In an effort to rapidly expand generation capacity, PLN entered into long-term PPAs with independent power producers (IPPs) through a take-or-pay scheme. These IPPs mainly use fossil fuels as their source of energy, and the take-or-pay agreements often range from 10 to 20 years. These contracts guarantee fixed prices and obligate PLN to purchase agreed volumes of electricity regardless of actual demand.

When power demand projections fail to rise to intended levels, PLN is forced to pay for unsold electricity. This is what’s been happening in the past decade: Indonesia suffered from an average oversupply of 33 GW caused by a mismatch in demand projection in 2015. Analysts estimate that for every gigawatt unsold, PLN incurs losses of roughly Rp3 trillion, placing a heavy fiscal burden both on the company and the country. Only recently, in 2025, did the ESDM Ministry reveal that the electricity demand in the island of Java and Bali, which makes up 70 percent of national energy consumption, had caught up with existing supply.

This leaves little incentive for the PLN to create new renewable energy plants. As a result, private parties remain dependent on the willingness of PLN to collaborate, creating a glaring bottleneck for realizing 100 GW worth of new energy.

In comparison, India, Vietnam, and China have implemented varying degrees of energy sector unbundling. In these countries, while the state retains control over transmission networks, private actors are permitted to compete more freely in generation and retail, allowing for greater renewable energy uptake. The results speak for themselves. As a result, these countries were able to capitalize on the 90-percent decrease in solar panel prices in the last decade because they understood the need for structural reform in their electricity sector. One could argue that Indonesia could easily catch up as well if the government is serious about achieving its stated goals.

Power wheeling could be an entry point to generate evidence of impact in reforming the market without immediately dismantling government control of the national energy grid. It allows electricity generators to sell power directly to consumers by paying a fee to use existing national transmission and distribution networks, without requiring the state utility to act as the sole buyer and seller. This provision is pushed for by renewable energy groups to be included in the New and Renewable Energy Bill, which remains stalled in parliament. However, because this act would allow for greater private sector involvement in the distribution of electricity, power wheeling remains contentious as it is seen as a step towards unbundling the electricity sector.

100 GW dream, one step at a time

Our message is that Indonesia’s ambitious solar power revolution is possible with proper planning and commitment to systemic reform. It should be about building the essential infrastructure for energy transition—from pricing distortions, resolving grid bottlenecks, sustaining access to financing, and creating an ecosystem where public and private partnerships can truly thrive. These may look less flashy, but will determine whether the ambitions manifest into reality or remain another pipe dream.