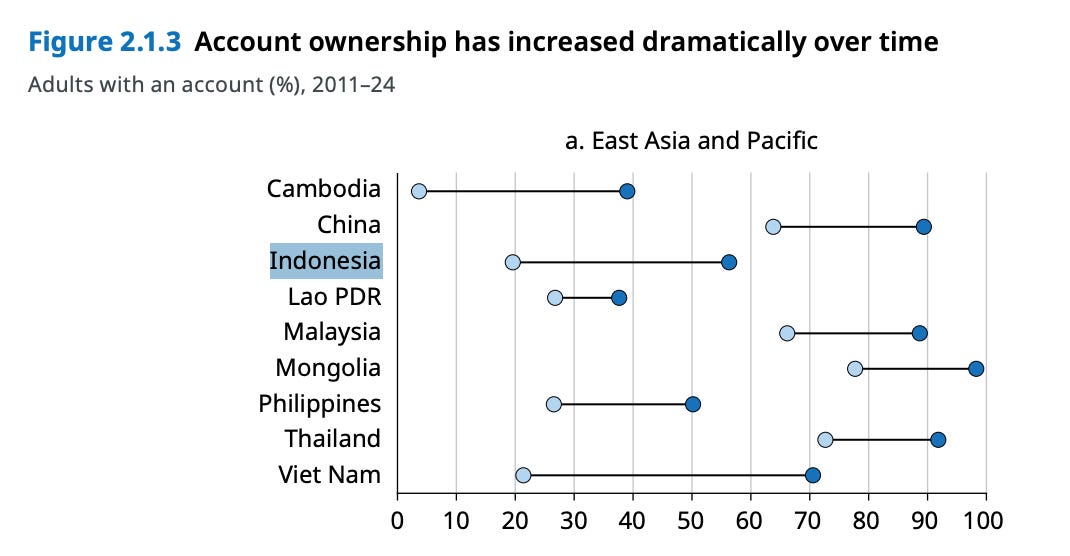

In 2011, the World Bank’s Global Financial Inclusion Index revealed that only 20 percent of Indonesian adults owned a bank account. Fast forward to 2025, the figure almost tripled by reaching close to 60 percent of the total adult population. The biggest contributing factor to this sharp increase? The growing digitalization of the country’s financial system.

While there is still much to be done, the goal of promoting financial inclusion can largely be attributed to the adoption of mobile banking and financial technology (fintech) systems, which allow a greater proportion of the population from diverse socio-economic backgrounds to participate in the formal economy.

The reform that best represents this change is the nation’s beloved Quick Response Code Indonesia Standard (QRIS), introduced by Bank Indonesia (BI) in late 2019. QRIS has become a lifeline by offering a low-cost and easy-to-use payment method for communities often left out of mainstream financial services. From your local street vendor to the most luxurious designer stores, it is difficult to imagine a merchant that does not have these iconic QR codes plastered all over.

In this edition of The Reformist, we trace the origins of QRIS, from its scattered beginnings to universal nationwide adoption, and how threats from the Western world emerged as QRIS continues to grow and foster greater regionalization across Asia.

From private sector innovation to state adoption

In the mid-2010s, the emergence of fintech applications laid the foundation of what would become the QRIS payment system. From 2017-2018, e-wallets like GoPay, OVO, DANA, LinkAja, and many more began experimenting with QR-based payments to their customers as an online alternative form of payment.

In August 2018, OVO even lauded their system, claiming that over 9,000 small and medium-sized enterprises had already begun using their QR payment services. Conventional banks such as Bank BCA, Mandiri, and BNI with mobile banking features were also involved in this digital renaissance of QR-based payment systems.

Ironically, during that same year, BI demanded that GoPay temporarily shut down its QR payment system for rolling out its services en masse without prior approval from the central bank. The same instance occurred with Bank BCA, which halted its QR code rollout after BI demanded that it do so.

The aftermath of these Payment System Service Providers (PJPs) crowding the market with their own sets of QR payment systems required consumers to have different applications installed, depending on which PJP provided a merchant’s QR code. During this period, it wasn’t uncommon for consumers to have multiple mobile banking and fintech applications downloaded on their phones just to prepare for a situation like this.

Realizing this, the government, through BI, decided to intervene in the market and integrate all the different mobile banks and e-wallets into one standardized QR code. This is not to say that the central bank selfishly co-opted private sector innovation, as BI worked closely together with the Indonesian Payment Systems Association (ASPI) to create the policy behind QRIS and its subsequent implementation, marking this reform as an example of proper public and private sector cooperation.

On Independence Day, 17 August 2019, through BI Regulation No.21/2019, QRIS was officially released by BI and became the universal QR code payment system for all banks and e-wallets, and came into effect on 1 January 2020.

Why QRIS won over the hearts of Indonesians

Even in its novelty, how has QRIS risen to such popularity? The clearest answer lies in its simplicity. Before QRIS, if cash was not readily available, debit or credit cards were the alternative. This, however, comes at the cost of having to purchase an Electronic Data Capture (EDC) machine, which would cost a merchant anywhere from Rp 1 million to upwards of Rp 5 million. With QRIS, merchants are required to pay a one-off registration fee of Rp 30,000 to create a unique code. Afterwards, the payment system requires only a functioning phone and a printout version of the QR code for consumers to scan.

Moreover, creating a financial account through digital banks or e-wallets has never been easier. There is no longer a glaring red tape where individuals are required to physically visit a bank branch to create an account, as it can now be done through a smartphone. Coupled with the fact that Indonesia ranks 4th in the world in total phone ownership at 187,7 million users, the push towards a digital economy is also a step towards financial inclusion. This especially rings true for rural communities with no direct access to conventional banking other than the outstretched reach of Bank BRI through its rural-based agent BRILink.

QRIS also isn’t just easy or practical; it has clear economic incentives that promote its use among domestic vendors. When QRIS was first rolled out, merchants were levied a 0.7 percent Merchant Discount Rate (MDR) on all their transactions, regardless of business scale. This changed when the COVID-19 pandemic struck, and BI slashed its MDR to 0 percent.

In July 2023, the MDR was once again re-implemented as social restrictions were lifted. Currently, micro enterprises are charged 0.3 percent for transactions over Rp 500,000, with anything below exempted from fees. Most businesses, however, fall under the small and medium-sized enterprises classification. These businesses are charged a flat rate of 0.7 percent on all transactions.

Price fluctuations aside, BI’s admin fees for QRIS remain comparatively low in comparison to debit and credit card MDRs. Under the National Payment Gateway (GPN), Indonesia’s interoperable bank framework, all domestic debit card transactions are capped at 0.15 percent for intrabank transactions and 1 percent for interbank transactions. Credit card transactions are levied higher fees as payment systems are managed through international issuers like Visa, Mastercard, and American Express. MDR fees can vary anywhere between 1.8 percent to upwards of 3 percent, depending on the card issuer and the merchant’s EDC provider.

Beyond economics, the impact the COVID-19 pandemic had on shaping a digital–based economy cannot be underestimated. With people unable to interact with one another in real life due to mobility restrictions, the economy moved remote, prioritizing online merchants and digital-based payments. This behavioral shift carried after the end of the pandemic as easy-to-use digital methods like QRIS became a preferred form of payment.

With all of these factors combined, it is only right to highlight QRIS’s statistical growth. At the end of its first year, QRIS logged 124 million transactions, with a total nominal value of Rp 8,21 trillion. Half a decade later, in 2024, that number has skyrocketed to over 6,2 billion QRIS transactions, totalling Rp 659,94 trillion in value. That is a 4,900 percent increase in transactions and a 7,938 percent increase in total transaction value. More recently, in September 2025, BI announced that the QR-based payment system had amassed 58 million users and 41 million merchants, 90 percent of which are micro, small, and medium-sized enterprises.

Realizing digital sovereignty amid threats from Western vultures

Since United States President Donald Trump returned to power early this year, international trade has faced headwinds through the introduction of his unilateral tariff policy aimed at reducing the US’s trade deficit. This has led to Indonesia being hit with a hefty 19 percent tariff on all goods exported into the US, as well as inviting further scrutiny of domestic policies that have affected US-based companies.

In April, the United States Trade Representative (USTR) classified QRIS and GPN as a non-tariff trade barrier to US-Indonesian trade relations. It argued that US-based financial giants Visa and Mastercard were not consulted when BI first created its QRIS regulation.

“U.S. companies, including payment providers and banks, noted concern that during BI’s QR code policymaking process, international stakeholders were neither informed of the nature of the potential changes nor given an opportunity to explain their views on such a system, including how it might be designed to interact most seamlessly with existing payment systems.”

This argument, however, fails to acknowledge that both companies have long been part of ASPI, who were heavily consulted in the creation of QRIS and continues to play a leading role in its implementation today.

The root of the problem predates the creation of QRIS. Through BI Regulation No. 19/8/PBI/2017, all domestic card transactions are required to go through GPN, mandating the use of domestic switching infrastructure. Under this ruling, foreign equity of switching institutions is capped at 20 percent, effectively sidelining Visa and Mastercard from establishing their own in-house operations. However, even if they were able to domesticate their switching system, their card-based model requires a radical change in behavior and an unrealistic fiscal barrier for local merchants.

Furthermore, controversies surrounding a high transaction fee of 2 to 2.5 percent have plagued Visa and Mastercard’s reputation in the US. Implementing such measures in Indonesia, when merchants are currently charged between 0.3 to 0.7 percent, would be simply untenable.

Friendly Asian countries and the internationalization of QRIS

While the US views Indonesian digital innovation as an adversary, the same attitude cannot be said for Indonesia’s friendly neighbors. In 2023, under the leadership of Indonesia, the Association of Southeast Asian Nations (ASEAN) pushed for greater international interoperability of each country’s QR payment system across the region.

The ‘ASEAN QR Code’ initiative saw Indonesia’s QRIS partnering with Thailand’s PromptPay, Malaysia’s DuitNow, and Singapore’s SGQR. These three countries remain the official partners that offer full interoperability with QRIS, offering a seamless interface and real-time exchange rates between currencies. Other ASEAN countries like Laos, Vietnam, Brunei, and the Philippines are also listed among the countries that accept Indonesia’s QRIS as a viable form of payment. However, the extent of their integration remains unclear, as BI continues to spotlight only the former three countries on its official channels.

At its core, QR interoperability between ASEAN countries not only eases international transactions but also promotes the direct exchange of local currencies between member states, reducing the region’s reliance on the US dollar.

Outside of Southeast Asia, the Indonesian government’s ambitions with its QR payment system have continuously expanded eastward. On this year’s Independence Day, BI announced that QRIS can now be used in Japan, albeit with a limited rollout to 35 official merchants. Concurrently, pilot tests in both China and South Korea are underway for QRIS to operate in both countries by 2026. BI also has its eyes set even further on India and Saudi Arabia as future targets for the QRIS market.

As Asia moves toward a cashless future, QR payment interoperability has fostered renewed regional cooperation built on a shared mission of financial inclusion, a collaborative spirit increasingly rare in today’s pragmatic international order.

What’s next for QRIS?

Since its inception, QRIS has continued to evolve year after year from its fragmented origins to international adoption. It is now experimenting with its new ‘QRIS Tap’ feature, where payments can be made by reading a smartphone’s internal Near Field Communication (NFC) chip on top of a card reader, making payments faster and easier than they already are.

Moving forward, sustained political will remains essential for both the central bank and government to ensure that every Indonesian has access to the formal economy. As it proceeds to grow, the Indonesian government must also remain firm in its stance to protect QRIS from foreign companies that will find ways to lobby their interests at the expense of the nation’s digital sovereignty. At the same time, the regional cooperation model proves that QRIS can expand internationally while preserving the principles of affordability and inclusion that made it successful.

After close to a decade of innovation and adoption, QRIS represents how policy reform isn’t always linear. Change does not have to happen from the public sector alone. When both the public and private sectors work together with a shared vision, private innovation can be uplifted through state promotion.

Correction Note: An earlier version of this article used the term ‘payment system’ too broadly to describe BI Regulation No. 19/8/PBI/2017. It has been updated to use ‘switching’ as per the BI regulation and USTR report. Switching refers to the network that connects different financial institutions, including banks and e-wallets, to process payments between them.

Ex-GoPay employee here. Thanks for the solid write-up! I still remember those days (circa 2019) when merchants had to have multiple QR code signs for GoPay, Dana, OVO, etc. like it was yesterday. The open secret was that we were all burning VC funding to compete for the same eyeballs but it was ultimately a race to the bottom. QRIS has undoubtedly been a solid regulatory FinTech intervention.